No Tax Returns?

No Problem.

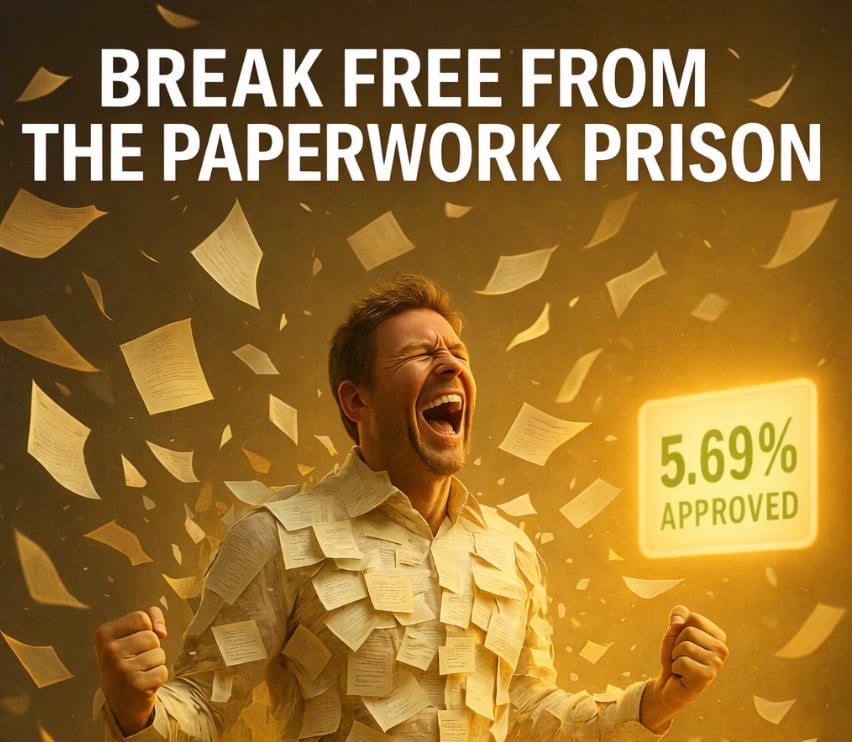

Self-Employed low-doc loans from 5.94%*—No Proof of Income Required.

Get answers fast — no tax returns, bank statements, BAS, or accountant’s letter needed when refinancing. Built for Australians without standard PAYG income or payslips, whether you're a sole trader, run your own company or just cannot prove your income.

Simple. No proof of income. Fair and fast.

Beat the Big 4's rate, with our low-doc 5.94% rate for business owners.

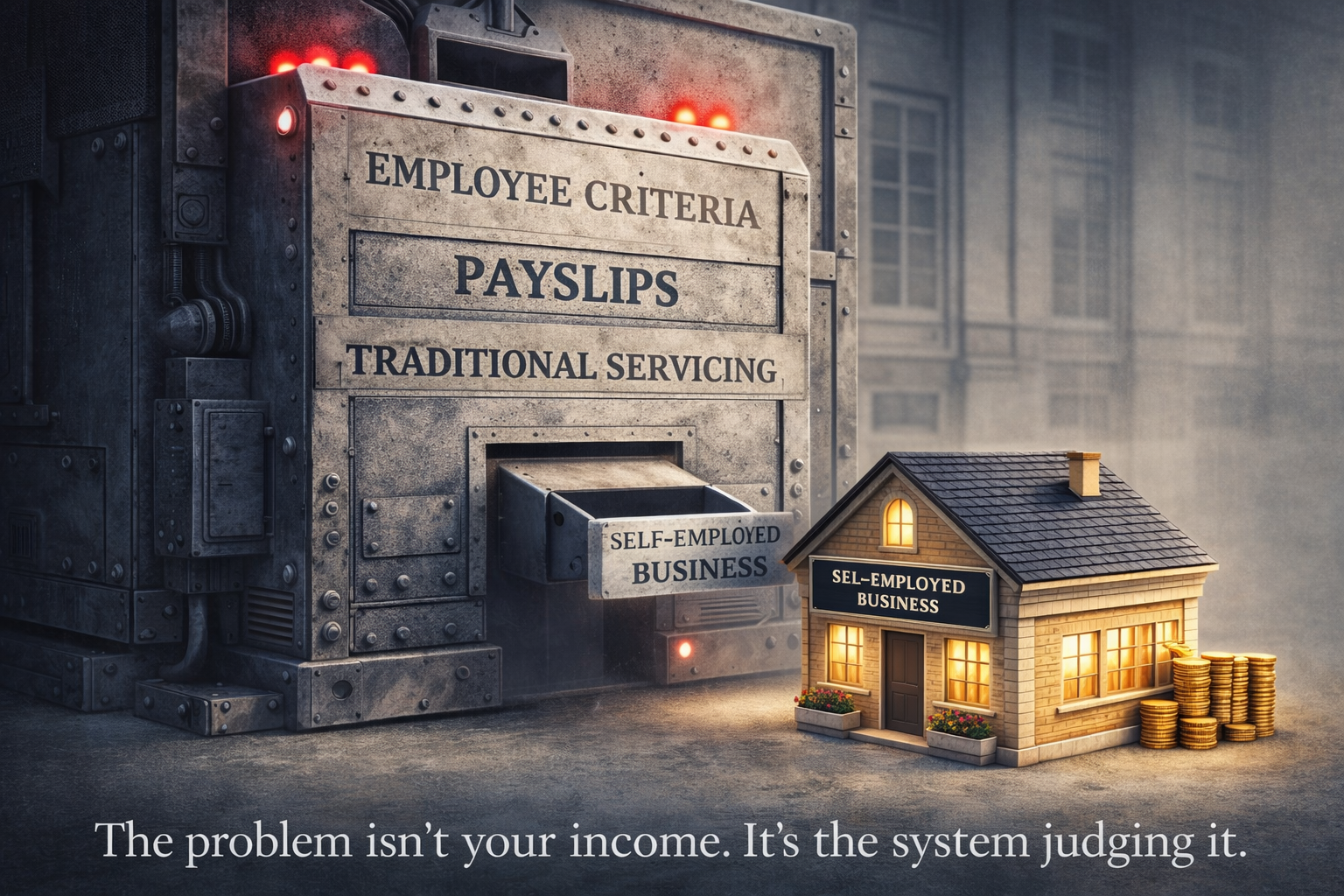

The Big Four Banks were built for employees.

Refinancing with them means pay slips, tax returns, and jumping through hoops.

Freedom Loans was built for ABN holders.

We can beat their rates — without requiring any proof of income when refinancing.

Flexible lending

Loans built around your business or non-standard income, non-restrictive lending designed for individuals.

Faster approvals

25+ years of relationships mean we cut through red tape for self-employed Australians.

Why choose Freedom Loans

Unique lending solutions for the self-employed or business owners of Australia.

No income proof

We understand self-employed & business financials don't always fit the banks "rules".

BIG4 beating rate

Lower rates mean more money stays in your pockets and out of the banks.

Faster approvals

25+ years of lender relationships mean faster decisions and better terms.

Years of savings

Reduce your loan term by years and save thousands of dollars n interest every year.

Our "no-proof of income" low-doc refinancing solutions helped 1000's of business.

How we helped everyday, self-employed Australians beat a corporate lending system designed to make it easy for the banks and get a better deal.

Your loan journey simplified

Three steps to unlock your lending potential

Choose Refinance or New Mortgage

Select the type of mortgage you want, and we apply the best rate possible.

We review your application.

We only process when you are 99% guaranteed of approval.

Go ahead, we process quickly.

We operate the fastest turnaround for qualified applicants

Common Questions

Common questions from self-employed Australians about low-doc loans

The mortgages come from different sources and therefore have different rates and lending criteria. We aim to refinance all new mortgages to the lowest possible rate in Australia after 12 months of perfect repayments.

Our aim is a 48-hour turnaround to review your application prior to lodgement. Most applications are processed quickly with our streamlined low-doc approach.

We don't require tax returns for our low doc refinancing loans, so no need to worry.

There are no hidden fees. The minimal fees are listed in the credit quote for you to review prior to moving forward.

Our initial check is a soft enquiry only. This does not affect your credit score as per the Equifax website.

We know navigating loans as a self-employed professional can feel complex. Our team cuts through the confusion with direct, honest answers tailored to your unique business situation.

Absolutely. We understand that business income fluctuates. Our lenders look beyond traditional metrics, focusing on your overall financial health and potential rather than rigid paperwork requirements.

Minimal documentation, for our refinancing, we only require 6-12 months mortgage statements, your rates notice and a credit score above 600.

Need more information?

Need personalised guidance?

Self-employed lending articles

If you can imagine it, we have funded it.

Get your personalised refinance or mortgage quote

Discover how much you could save with our no-proof, low/no-doc loan options